Trump’s Trade War Is Back—Bigger, Blunter, and More Dangerous, but...

We are no longer debating whether the trade war ever ended. We are living in its escalation.

“Tariffs can buy time. But they cannot build a future. Only vision can do that.”

President Donald Trump has imposed a universal 10% tariff on all imports and layered additional country-specific tariffs—34% on China, 24% on Japan, and 20% on the European Union. He cited economic sovereignty, competitive rebalancing, and "restoring American greatness" as the rationale. What was once campaign rhetoric has matured into full-spectrum trade doctrine.

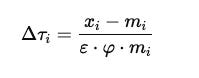

At the heart of this policy is a deceptively logical formula:

Where:

In simple terms: the larger the trade deficit with a country, the higher the tariff—adjusted for how badly we need their goods and how much consumers will absorb in price hikes. This economic model, likely derived from trade theorists advising Trump's first-term policy hawks like Peter Navarro, now serves as a framework for real-world action.

But formulas do not govern global trade—relationships, supply chains, and consumer behavior do. And as these new tariffs take effect, the consequences are mounting fast.

The Real Costs of Escalation

Consumer tech has already taken a hit. Tariffs on Chinese electronics are forcing price hikes across the board: smartphones, laptops, and smart TVs are expected to rise 20–50%, with manufacturers like Apple and Samsung revising Q2 earnings downward.

The auto industry is bracing for disruption. Foreign-made vehicles, including those assembled in U.S.-based plants by Japanese and German automakers, now face an effective 25% cost penalty. Dealers are forecasting slower summer sales, and electric vehicle adoption—already facing battery supply constraints—is at risk of stalling.

U.S. agriculture is once again in the crosshairs. China's 15% retaliatory tariff on soybeans threatens $12.8 billion in annual exports, disproportionately affecting farmers in swing-state economies. This mirrors the fallout from the 2018–2019 trade war, when soybean exports to China collapsed by 75% and led to $28 billion in federal bailouts.

Markets Are Responding

Wall Street is already reacting with unease. On April 3, the S&P 500 dropped 4.9%, its steepest daily decline since the 2020 COVID crash—wiping out $2.5 trillion in value. Inflation forecasts are now 2.2% higher than previous CBO estimates, driven by tariffs on goods that have few viable substitutes in the domestic market.

While the administration promises these tariffs will spark a manufacturing renaissance, history offers a different lesson. In the wake of the first Trump tariffs, the U.S. saw minimal manufacturing gains, but significant price increases. A Federal Reserve study from that period found tariffs cost households $1,277 per year, with no statistically significant uptick in job creation.

Global Fallout and Diplomatic Drift

The geopolitical repercussions are swift and sharp:

China is mobilizing retaliatory measures.

The EU and Japan have filed formal WTO complaints.

ASEAN countries, caught between Beijing and Washington, are diversifying away from both—accelerating the fragmentation of global trade.

This isn’t just a policy dispute—it’s a strategic turning point. If these tariffs remain a permanent fixture—as some in the administration hope—they risk locking the U.S. into a zero-sum, transactional model that undermines long-term cooperation, innovation, and economic leadership.

Yes, the U.S. trade deficit with China has narrowed—but that doesn’t mean trade is “fixed.” It simply shifted elsewhere, to Vietnam, India, and Mexico. Global trade hasn’t shrunk. It’s reshuffled.

And despite the optics, the jobs haven’t come back. What we’ve gained in symbolism, we’ve lost in strategy.

A Smarter Strategy Exists

This isn’t a call for surrender. It’s a call for strategic discipline—and long-term thinking.

The truth is, tariffs alone won’t reshape the American economy. They may block goods, but they don’t build capacity. They may protect select industries, but they don’t develop talent or spark innovation.

If the goal is true economic competitiveness, we need to think bigger than border taxes. We need to invest in the foundations of modern productivity, starting with:

Semiconductor manufacturing: The CHIPS Act set the stage, but execution is everything. The U.S. must scale domestic fabrication, support foundries, and invest in supply chain security for critical inputs like rare earth elements and advanced lithography equipment.

Artificial intelligence and clean technology: These sectors will define the next industrial age. Regulatory clarity, federal procurement, and public-private R&D partnerships are essential to attract capital, talent, and first-mover advantage.

Workforce development: We cannot outcompete global rivals if our labor force isn’t ready. This means apprenticeship programs, STEM education, reskilling for high-tech manufacturing, and immigration policy that welcomes global talent.

If the goal is global leverage, we need modern trade architecture—not just tariffs and threats. The U.S. should be:

Leading digital trade agreements that set global norms for data governance, privacy, and cross-border e-commerce.

Crafting reciprocal trade deals focused on intellectual property protections, especially in the biotech, software, and entertainment sectors.

Aligning trade policy with climate strategy, using green industrial standards as both economic stimulus and diplomatic tool.

Put simply: we need a strategy that moves from reactive protectionism to proactive economic statecraft. Tariffs may signal strength—but only investment builds it.

The Pros and Cons of Trump’s Tariff Doctrine

To fairly evaluate the current trajectory, we need to weigh what’s working—and what’s not.

Pros:

Signals resolve: Tariffs demonstrate a willingness to challenge countries—like China—that have long benefited from asymmetric trade terms.

Buy-American momentum: The policy has reignited public and political interest in domestic manufacturing and supply chain security.

Negotiating leverage: Tariffs can serve as a stick in trade negotiations, forcing concessions or opening restricted markets.

Cons:

Higher consumer prices: From electronics to food, tariffs raise costs that are ultimately passed to American consumers.

Retaliation risk: As seen with China’s soybean tariffs and EU complaints, unilateral action invites countermeasures.

Minimal industrial return: Despite political narrative, most data show limited manufacturing job growth tied directly to tariffs.

Global fragmentation: Overreliance on tariffs strains alliances, encourages trade bloc formation, and reduces U.S. leadership in multilateral trade bodies like the WTO.

In short, Trump’s approach has stirred the right questions—but not always delivered the right solutions.

In Conclusion

Trade is not a scoreboard. It’s a system. And systems don’t reward symbolism—they reward design.

If the U.S. wants to lead in the global economy of the 21st century, it must do more than tax the past. It must build the future.

Tariffs can buy time. But they cannot build a future. Only vision can do that.